Main Takeaway: Central banks are hiking rates at warp speed. There is a growing consensus among experts that this aggressiveness is so that central banks have the power to decrease them when a recession hits. That said, be prepared for rates to push well passed the 8% mark in the short term.

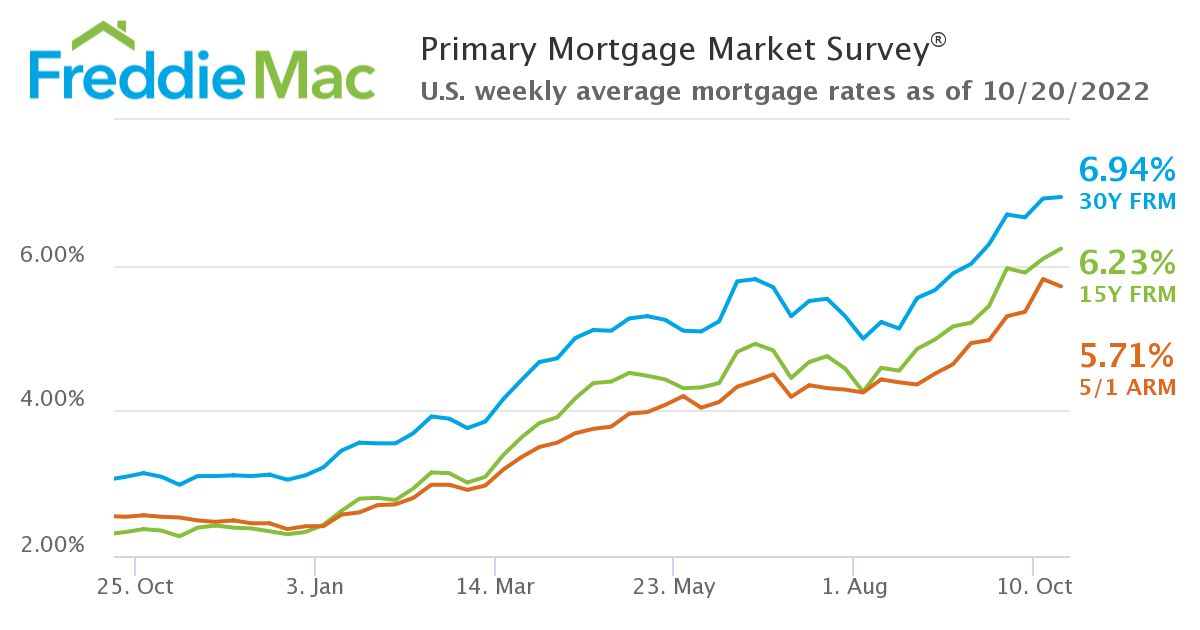

Story: The 30-year fixed rate is fast approaching 7%, and the Federal Reserve is expected to continue raising its benchmark rates in the near term.

Source: Freddie Mac

This has many in the multifamily industry worried about rising debt costs and an inability to acquire new assets until price increases decelerate significantly, or decline. Here’s what multifamily owners and investors need to know about the current interest rate environment.

How high will interest rates go?

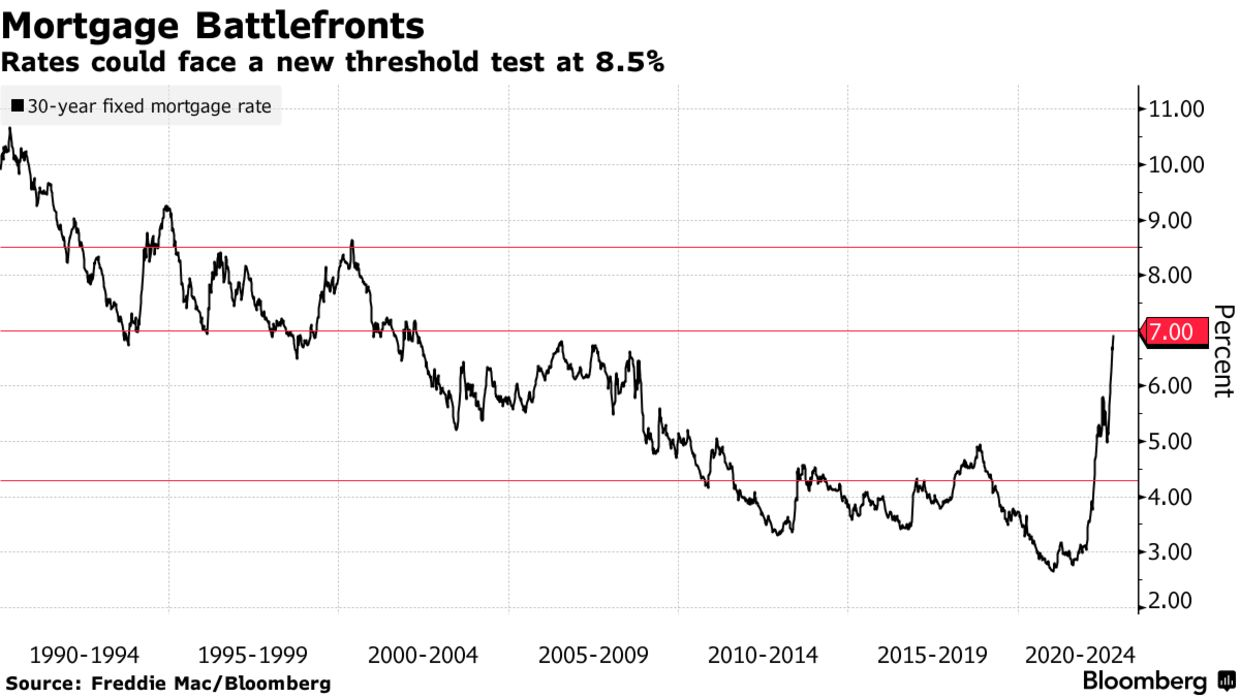

If you listen to the experts, likely above 8% in the short term. According to Lawrence Yun, chief economist at the National Association of Realtors (NAR), technical analysis shows that once rates push above 7%, they will likely go to 8.5% in the near term. Yun likens the 7% threshold to an army breaking through the front lines, and once a breakthrough is made, a strong advance will follow.

Further, at their next meeting in early November, fed funds futures are now giving a 90% chance that the raise will be 0.75%. The Wall Street Journal (WSJ) reported recently that they agree that the November meeting will result in a 0.75% increase.

The goal is to slow economic growth to keep inflation down, but strong labor, housing, and consumer markets have kept inflation stubbornly high. That said, we are seeing the level of mortgage volume decrease significantly which will have a chilling effect on consumer equity and home prices heading into 2023.

According to Freddie Mac, home purchase originations are expected to sit at $1.9T by the end of 2022, and $1.6T in 2023. To compare, originations were $2.0T in 2021. The cooling is here.

When will interest rates start going down?

There’s always a silver lining, and in this story, it comes in the form of a recession. Once a recession hits, central banks need the firepower to drop rates to help improve recessionary pressures.

According to the WSJ: “Fed Vice Chairwoman Lael Brainard and some other officials have recently hinted at unease with raising rates by 0.75 points beyond next month’s meeting. In a speech on Oct. 10, Ms. Brainard laid out a case for pausing rate rises at some point, noting how they influence the economy over time.”

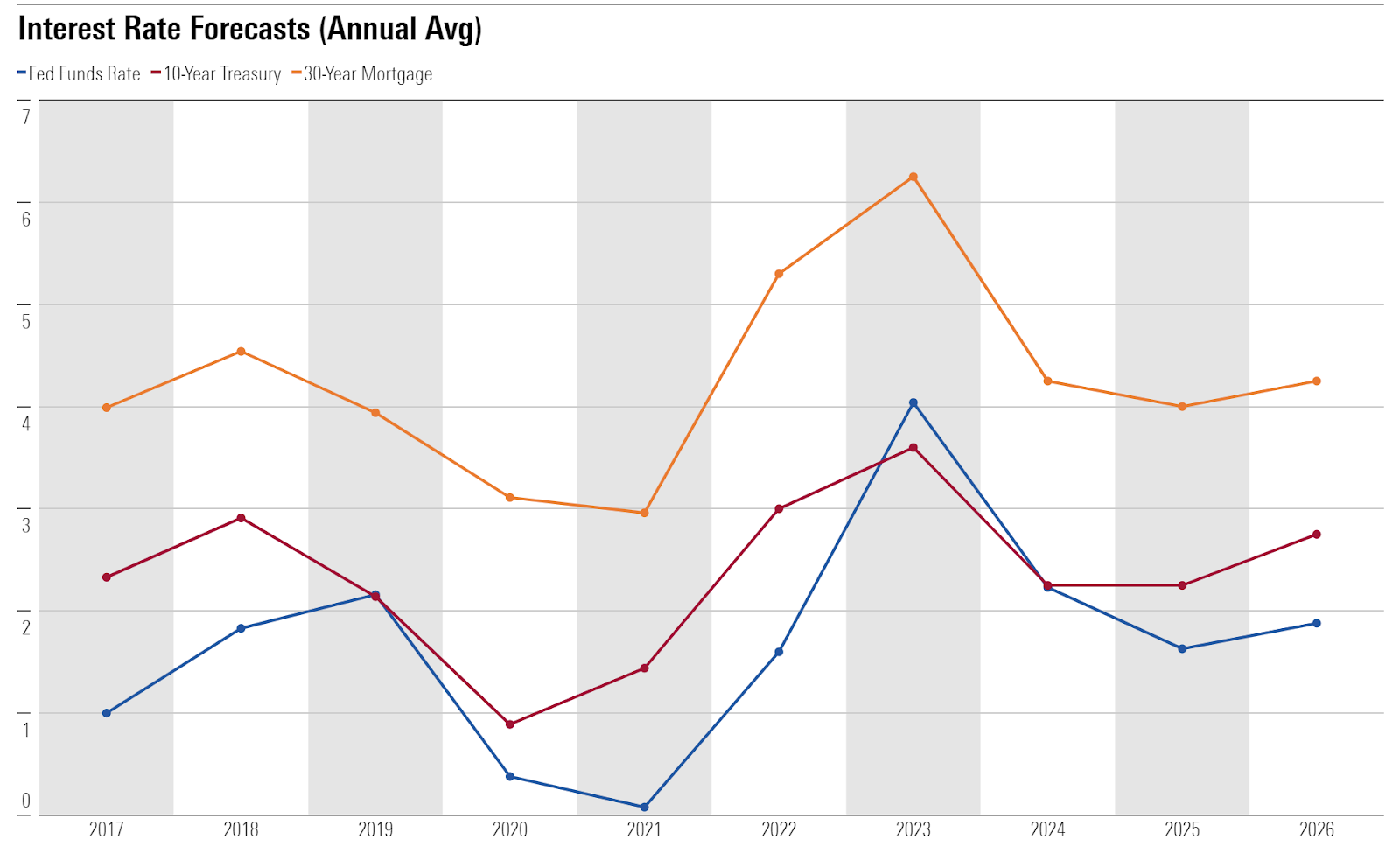

In Morningstar’s 2022 U.S. Interest Rate & Inflation Forecast, they conclude that:

The U.S. Federal Reserve is expected to pivot to ease monetary policy in 2023 as inflation falls and the need to shore up economic growth becomes paramount. Morningstar’s current 2026 projection for the federal funds rate is 1.75%, though rates are to dip below this level in 2024 and 2025. Due to the unwinding of price spikes caused by supply constraints, inflation is expected to swing from inflationary to deflationary by 2023, which means curtailing inflation will be much easier.

This appears to be good news for multifamily owners. Already in neighboring Canada, the central bank is decelerating rate rises. On Wednesday, the Bank of Canada increased its benchmark rate by only 0.5% when many expected 0.75-1%.

The cause of a dropping benchmark rate? Decelerated inflation. Morningstar predicts that inflation has peaked, and will dramatically decrease to 2.6% in 2023, and 1.4% in 2024.

Other experts tend to agree with the thesis that rates over the coming years will come down. According to Motley Fool, Fannie Mae predicts that 30-year mortgage rates are going to average 4.5% in 2023, the Mortgage Bankers Association (MBA) sees mortgage rates at 4.8% by 2023, and NAR sees rates of 5.5% by next year.

Expert take on when interest rates will go down

“Underlying multifamily fundamentals are still strong and returns have been excellent. Housing is still undersupplied and the cost to own versus rent has never been larger…While we may see a temporary pause, as soon as market stability returns, investors will feel comfortable deploying capital in one of the best inflation hedge asset classes.” — Kelli Carhart, head of multifamily debt production for CBRE

“In the long run, the Fed largely disappears from the picture. Instead, interest rates are determined by underlying currents in the economy, like demographics, productivity growth, and economic inequality. These forces have acted to push down interest rates in the United States and other major economies for decades, by creating an excess of savings over investment. In other words, the natural rate of interest has shifted downward.” — Preston Caldwell. Morningstar