Main Takeaway: The key to success for proptech is not the dizzying amount of VC funding it has enjoyed over the years, but its adoption levels with owners and operators of the real estate assets. The funding environment for proptech will be strained in the coming years, forcing those who will survive to be laser-focused on efficiency and revenue.

Multifamily owners and investors can take a valuable lesson in this approach as inflation and interest rates continue to increase, and many trends in proptech can help them solve for greater efficiency and improved tenant experience.

Story: Talks of a recession, inflation, and investment capital drying up would have many assuming the property technology industry is in for some pain. They may be wrong. The pandemic has certainly fast-tracked digital transformation in all industries, including real estate, but the stability of proptech goes well beyond that.

The State of Proptech 2023

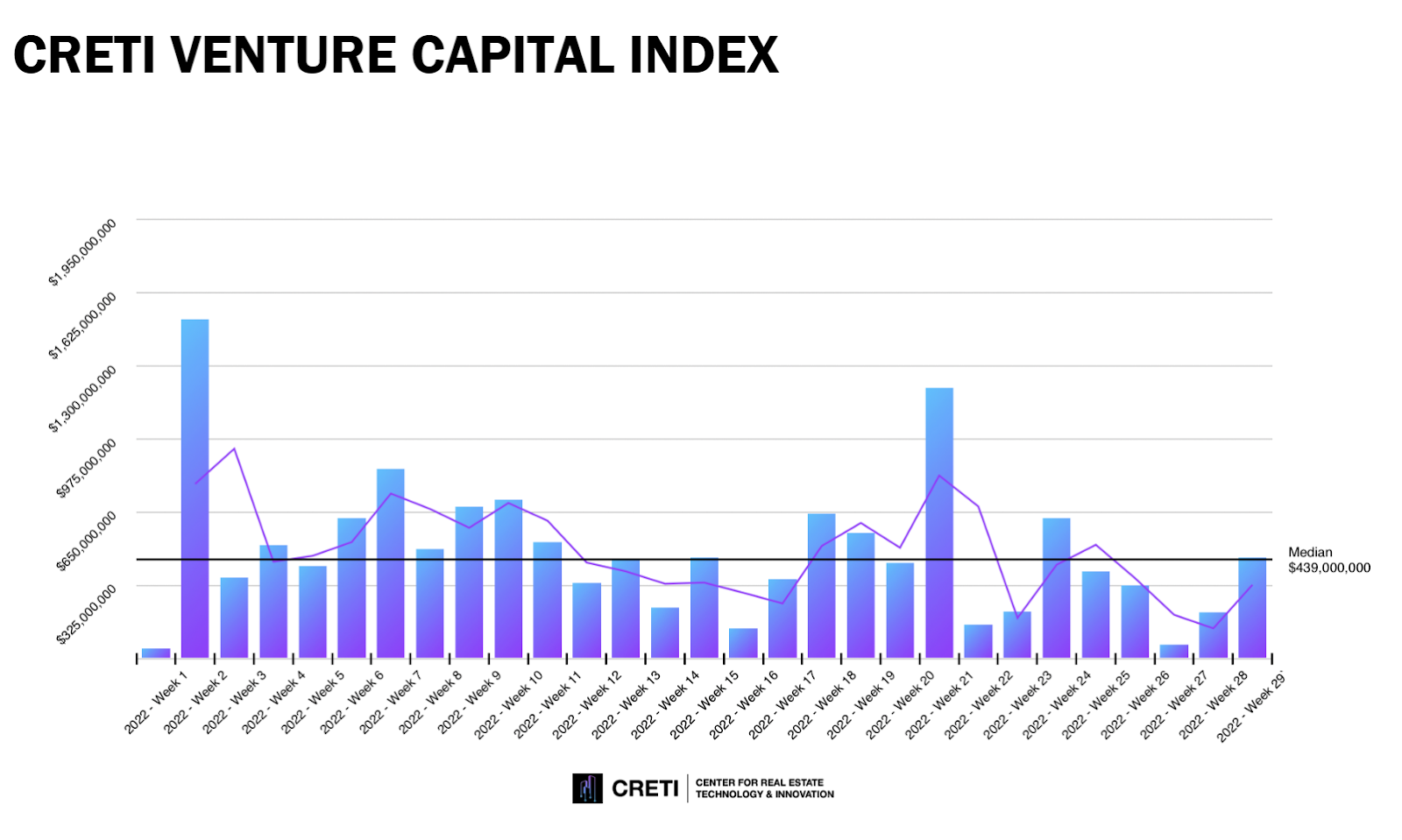

The Center for Real Estate Technology & Innovation (CRETI) reported an increase in real estate tech investment in 2022. In Q1 and Q2 of 2022, $13.1 billion was invested in proptech companies. This was a 5.6% jump in funding year-over-year. As you can see, venture funding in proptech has not entirely dried up:

Source: CRETI

Indeed, a recent proptech survey found that 87% of investors said they will exceed their 2021 investment levels. What’s more, a record number of these investments were made by real estate firms and operators themselves, showing a growing maturity and a literal buy-in to the necessity of technological adoption.

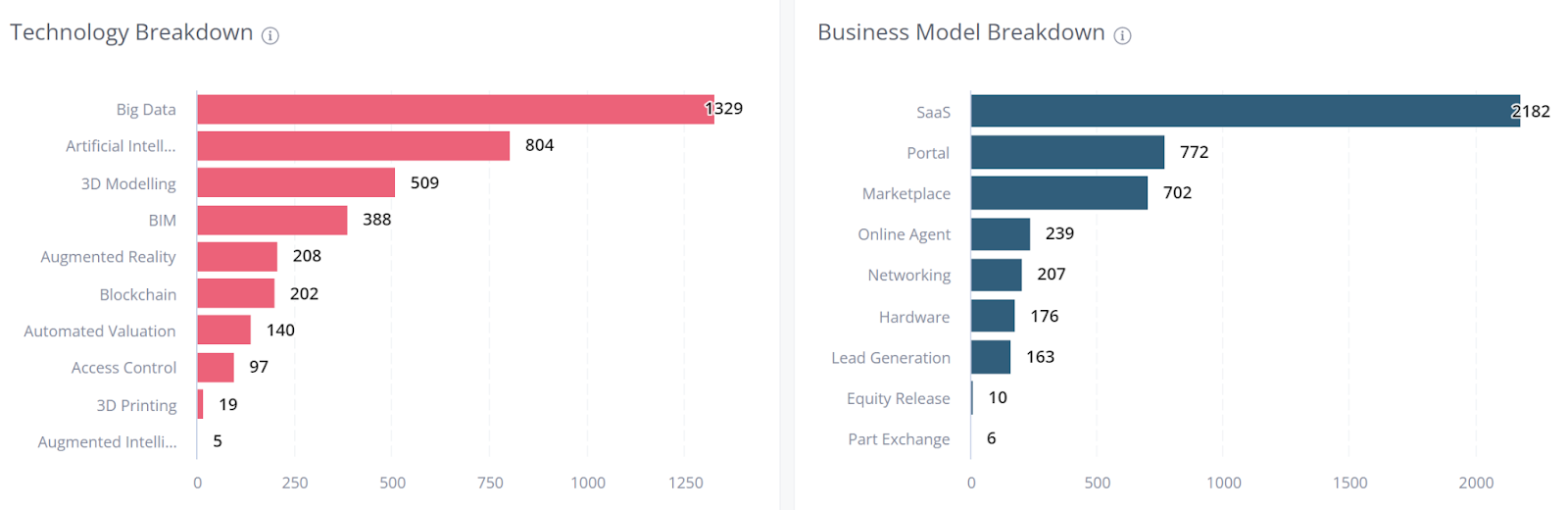

According to Unissu, there are almost 10,000 proptechs globally, split almost evenly between commercial and residential markets, with over 2,000 located in the U.S. Here is the breakdown of the type of technology and business models of global proptechs:

Source: Unissu

In fact, during a time when venture capital is significantly drying up, Fifth Wall just announced a new $500 million fund focused on proptechs helping to de-carbonize the real estate industry. Here are some of the larger trends owners and operators should be aware of as we enter recessionary headwinds and evolving consumer demand.

The Biggest Proptech Trends in 2023

M&A – Mergers and acquisitions will be a significant proptech trend in the coming years as valuations get depressed and more technology is consolidated into complete solutions. We’ve already seen some of this with JLL’s acquisition of Building Engines, VTS’s acquisition of office experience platform Lane Technologies, and Fortive’s purchase of facilities SaaS company ServiceChannel, just to name a few.

Legacy – One of the biggest opportunities for both proptechs and multifamily owners is in retrofitting aging and legacy buildings. As borrowing costs and cap rates increase, asset owners will increasingly look for creative ways to optimize and monetize their properties.

This can be done through a combination of smart access, tenant experience applications, sensors, and upgraded infrastructure such as internet and wifi. Although an upfront capital expenditure, these additions over the long-term can improve NOIs as well as tenant experience which improves asset values and occupancy rates.

Indeed, Ryan Masiello, co-founder of VTS summarizes this trend: “We’re in the early stages of a modernization boom for the industry, where landlords are spending more or will be spending more offensive capital in the next two years; probably more than they have in the last 10. In order to support that and make sure that people can interact with the experience they’re trying to create, the building obviously needs technology to do that. So tenant experience has been really the focal point for the industry.”

Key Sectors – Proptech has dozens of sectors looking to digitize and automate various aspects of the real estate supply chain and consumer experience. That said, a few sectors will shine as both commercial and residential tenants look beyond simply having space, they want an experience and reduced friction.

- Environment: The built world is said to contribute around 40% of the total carbon emissions. Proptech has been tackling this issue with a number of innovations in the fields of energy consumption, circularity, off-site construction, and mobility, among others.

- Smart Access: Cloud-based smart building access solutions will be the new normal among multifamily assets. These innovations help elevate the resident experience, reduce operational burdens for property managers, and maximize NOI for building owners.

- Construction: As labor and supply constraints continue, digitizing constructions and development will help alleviate the ongoing pressure on starts and completions.

- Office: As the return to normal office operations remains in flux, residential owners and operators will need to implement more work-friendly amenities and technologies such as improved connectivity, physical and cyber security, flex office space, meeting rooms, and more.

Proptech Experts

Matt Knight

“I expect a renewed focus on cost control and FinTech. With mortgage rates (at best) uncertain and many lenders simply leaving the market, owners and managers will need to tidy up their FinTech stack to cut costs and manage potentially more-complex debt and equity structures. For cost control, I’d bet you see more of the energy, water, and tax technologies receive renewed attention. If the past decade has been about growing revenue, the coming year will be about cutting costs.” — Matt Knight, proptech investor, and owner of Vertical.

Michael Beckerman

“Now more than ever we are clearly in a market cycle that will see the proptech startup ecosystem begin to separate between those solutions that are a “nice to have” and those that are “must have”. Just as covid was a tremendous technology accelerant in the real estate sector, the challenging economy, supply chain issues, and labor shortages that are confronting every industry today, but particularly the real estate sector, will drive adoption to those startups that are helping solve some of these challenges. As a result, and given the slowdown in venture funding, we will clearly also see a great deal of consolidation in the sector which is a good thing for real estate owners who have been frustrated for years by the lack of integration and single-point solutions available in the marketplace.” Michael Beckerman, CEO, CREtech

Sarah Liu

“While the funding numbers for proptech look like they are still holding strong, it’s important to keep in mind the lag between when rounds close and when they are announced, typically 3-6+ months later. On the ground, we are starting to see a slowdown in investment activity that will likely be reflected in public data in the latter half of 2022. That being said, while round sizes, velocities, and valuations have responded similarly to those in the broader technology market, the underlying need for technology in the Built World remains as strong as ever. While rising interest rates and a potential looming recession may decrease overall development and transaction activity, I expect tech start-ups that drive real ROI to increase their penetration and market share as owners, operators, and managers seek ways to protect against compressing margins and cap rates.”— Sarah Liu, Partner, Fifth Wall

“Now more than ever, landlords must prioritize smart technology that preempts the changing requirements of those occupiers interacting with it…Landlords need to understand how technology positively impacts not only their own goals, but the goals of their occupiers.” — Arie Barendrecht, founder and CEO, WiredScore